Singapore Retail Segment is facing headwinds from eCommerce, most malls now have cater to more F&B outlets. However China's retail segment has a better prospect as middle class grows and spend more.

Comparing from the past results against 1st Quarter results, the recent placement (an increase of 10% shares) has diluted the DPU. the current DPU is supported by the capital distribution from a portion of the gain from the disposal of Anzhen. Probably why the price tanked since FYQ4 results was released.

2nd Quarter results, Rock Square provide full quarter contribution. DPU increases with capital distribution from a portion of the gain from the disposal of Anzhen.

Forward looking: The Joint venture acquisition of Rock Square reported renewal revision of more than 20%. More than 50% of expiring leases are expect to renew from 2018

to 2020.

DPU has a CAGR of 13.34%. Recent drops relates to the implementation of value added tax, divestment of Anzhen and the placement of shares.

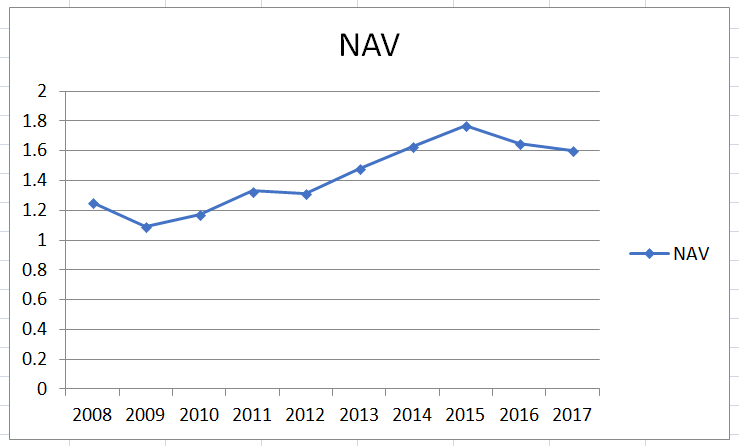

1HFY2018 DPU of 5.39cents, assuming full year DPU of 10.76 cents which gives a current Yield of 7.3% with the price of S$1.47. Gearing is at a healthy 32.1%, interest coverage of 5.9x, PB ratio at 0.86.

1HFY2018 DPU of 5.39cents, assuming full year DPU of 10.76 cents which gives a current Yield of 7.3% with the price of S$1.47. Gearing is at a healthy 32.1%, interest coverage of 5.9x, PB ratio at 0.86.

0 comments:

Post a Comment