Sembcorp Industry(SCI) has been hammer down since 2016. Main Business is with the Utilities and Marine sector. Oil has plunged to below US$40 in 2016, bump up to US$74 and now back to US$40ish. and so has the share price. The share price is now $2.51 compare to 2016 low of $2.56. Yes, it is even lower now with a new low of $2.43. In terms of Price to book value is at 0.64x, at this price you get the marine segment for free. The book value of the marine segment is 31% of SCI's. This a bargain! However SCI results are still worsening, Net margin are getting pathetic. Debt are increasing since 2010. Interest cover is at 2x but current ratio is at 1.1x with quick ratio at 0.68x. Hence this could further dampen the stock price, especially with the current economic outlook. Oil is still being heavily manipulated. After 3 long years, Oil prices never recovered to near US$100.

Will SCI go bust? It is owned by Temasek Holdings (Private) Limited with 49% stake. Anything can happned doh. I find cyclical stock are hard to invest in. Base on book value, it seem to be a bargain. Well you don't get to buy at bargain unless things are bad right?

I bought Tat Seng Packaging(TSP) last year before I start writing this blog journal. Sometimes I re-read my own post to remind myself why I bought in the first place and not to panic. Hence I have been wanting to do a write up. TSP business is very simple, producing packaging products such as corrugated paper boards, corrugated paper cartons, die-cut boxes, assembly cartons and heavy duty corrugated paper products. Customers are from sectors includes food and beverage

industry, electronics and electrical industry, plastic and metal

stamping industry, pharmaceutical and chemical industry as well as the

printing, publishers and converting industry.

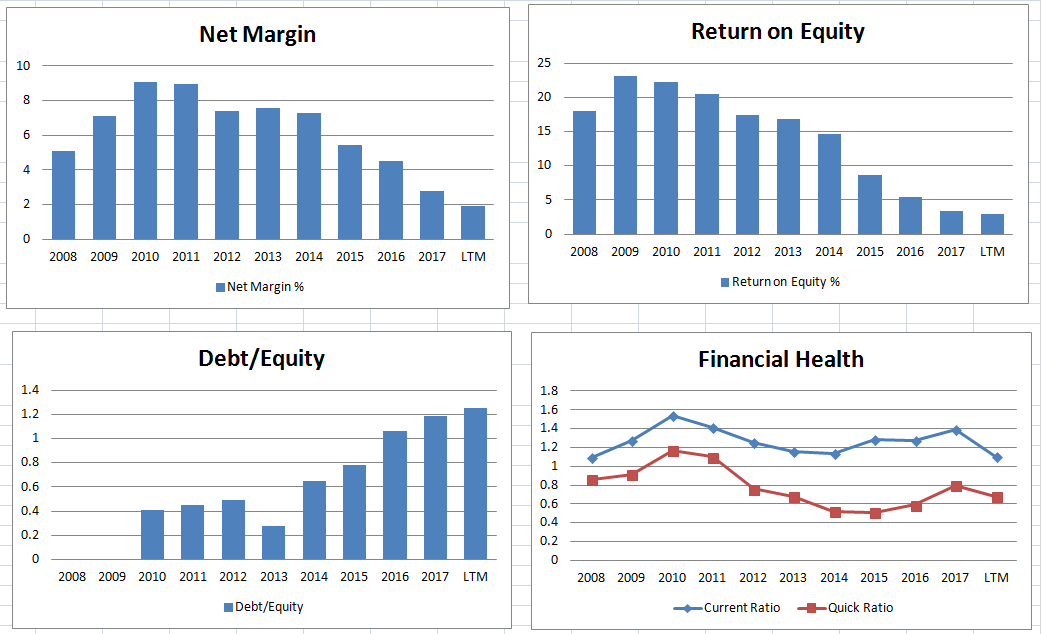

TSR is growing at an a impressive CAGR of 13.62% over the last 9 years. Net margin is growing as well which mean more profits and increasing dividend as EPS grows. ROE is at a record high of 20%. The standard FCF = Net profit - CAPEX, when calculated give a very bad picture. FCF drop drastically due to the cost require to build a new plant in Nantong. If we look at actual cash flow a company has in their disposal, Actual FCF = Net profit - CAPEX - Investing activities + non-cash items + Borrowings during the fiscal year. In 2017, we can see an increase in debt which helps to boost the cash flow. However Debt/Equity is near 52%, which is still low. Interest Cover is at 30x.

Business Moat

I would say TSP no business moat for the business, there are more than 5000 similar companies in china. Therefore it really up to how the management manage the business. Cost management, efficiency, productivity such as being one of the few that operate 24 hrs , the capacity to increase production during big event like 11.11 singles day sale. (Your can read more from AGM 2017 post) Having private china investor helps too in terms of business relations.

Business risk comes from higher raw material cost if they are unable to pass on to their customers (they are able to, to some extend mention during the AGM 2017). Slow down in economy, maybe due to the trade war. However all these are short term risk, with current and quick ratio are above one, the business has the financial strength to weather through.

Cash Cover Conversation Cycle

Receivable over Sales seem high, at around 40% but the Cash Cover Conversation Cycle (CCC) was below 0. This means that the company take a longer time to pay out than their customer to pay them which is good. However the LTM 2018 see CCC spike back up to 2008/2009 levels. This show the customers need more time to pay up, also show that they have become more conservative in keeping their cash flows. In this case, TSP also pay out faster than usual.

Trading at S$0.59 with a NAV of $0.79, PB ratio is at 0.75 and 4x PE. Dividend yield is at 5%. The current price seem reasonable.Vested at S$0.72 :(

I had looked at Mapletree North Asia Commercial Trust (MNACT) when I started investing in late 2015. However a few reasons make me reluctant to invest in it then. High Gearing At almost 40% which may result in rights issues.Over the years I have learnt that rights may not be bad and give a good chance to buy more at a cheap price like the recent Frasers Logistic & Industrial Trust Rights issue.Most Mapletree Reits has high gearing. So it is unavoidable. Over the years since 2015, gearing still as high near 40%. Most of time, they issue placements rather than rights. Young Reit listed less than 6 years ( 3yrs in late 2015) Only 2 Properties in 2015 It had since grow to 9 properties

Festival Walk (Retail + Office, Hong Kong)

Gateway Plaza (Grade A Office, China )

Sandhill Plaza (Business Park, China)

6 Japanese Office Properties (Chiba, Tokyo, Yokohama)

MNACT to me is like a mirror of Mapletree Commercial Trust (MCT) but in oversea properties with Festival Walk as its core just like Vivocity with MCT. Festival Walk

Festival Walk is located next to City University of Hong Kong, with ample nearby estates as well as international schools (Need to Zoom in Google maps to have more displayed). I believe these schools will attract properties demand and hence more people staying nearby Festival Walk and more footfall. The Kowloon Tong MTR is located nearby with a walkway link to Festival Walk. Festival Walk contribute 63% of MNACT Net Property Income.

DPU Growth

The manager did a good job growing the DPU which has been increasing with a CAGR of 4.65% for the past 5 years. Occupancy and Rental Performance

The occupancy rate at Festival Walk is amazing, keeping at 100% whereas the rest is pretty good too. Positive rental reversion for the last 4 quarters is also show a very good results. Expects room for further yield improvements for the Japan properties as some of the leases are currently under-rented (Source). Lease expiry for the next 2 years mainly come from Festival Walk but I think it won't haven any issue getting 100% occupancy rate.

Gearing Gearing is at 39%, however analyst expects this ratio to fall when its existing portfolio of assets

are revalued at the end of FY18, particularly given the sharp rise in

asset values in Hong Kong. (Source) Conclusion I like how MNACT have performed and grew over the years, DPU has been growing nicely. 1H2018/2019 Dividend is 3.807cents, 2H usually give a slightly higher dividends. Estimating a full year dividend to be 7.707cents, at a price of $1.10 gives a yield of 7%. PB ratio of 0.83. Risk for this Reit will be of the weakening of foreign currency against SGD as well as the economy of that region. And Festival Walk contributed 63% of Net Property Income which is a concentration risk as well. Vested @ 1.09

CapitaRetail China Trust (CRCT) Q3 results give a few positives. This show that China's domestic consumption is strong as the middle income grows. Results also show rise in shopper traffics and sales of tenants. DPU increase 1.7% Y-on-Y, YTD DPU of 7.8cents present a 7.7% yield at the price of $1.36. Debt has been refinance and hence no refinancing needed till 2020.

Rental reversion Rental reversion is tremendously high for properties acquired in 2017, CapitaMall Xinnan and Rock Square.

Conclusion Gross revenue has fallen YTD 2018 in terms of SGD however NPI( Inluding Joint Venture Rock Square) has approximately the same as YTD 2017. However, Distribution amount is higher in 2018. This is likely because of the distribution for the divestment of Anzhen.

So once this distribution from Anzhen eased, DPU should drop. I believe CRCT's management is confident the rental reversion will continue to increase to cover up the difference.

CRCT's NAV from Q2 $1.71 to $1.57, PB ratio is now 0.87. This is maybe due to depreciation of the RMB. Gearing at 35.7%, Interest cover 5.9x.

I was skeptical that the AEI can contribute much to the DPU. Q1 StarhillGbl Reit FY2018/201, DPU drop 4.2% to 1.15cents Y-on-Y. Some people mentioned that its an increase Q-on-Q. However, past years DPU shows that Q1 always give out higher DPU and Q4 the least. Hence we cannot compare Q-on-Q.

Upon facing more decline in DPU, StarhillGbl Reit also has more than 1/4 of its lease expiring in this new fiscal year. This is a huge amount of lease, tenant move out will be bad news. Keeping the rental reversion flat is also bad for shareholders.

StarhillGbl Reit performance has been bad for consecutive for the 3rd year. AEI doesn't improve the DPU. Huge expiring leases. Probably will avoid this reit, if I have to set a TP, base on a further decline of 4-5% this year, with 10% MOS, it gives a TP of $0.575.

This write up is overdue as I bought IGG in May 2018. Owning a game company just got Complicated due to China's freeze in new game approval. As a gamer and now an investor, owning piece of a game company is a great idea, since I can't make or work in one. I have looked around US and Japan. I probably miss some companies in my watch-list but not all game companies are doing great (sega, konami, capcom, nintendo). Those that are doing well (Squarenix, Activision Blizzard) are overvalued. During a stockcafe's screener in May, the result gave me an interesting list. I looked through all of them and an mobile gaming company appears in it. IGG inc, I GOT GAME is a mobile game developer, just like Tencent. The Gaming Industry The Global gaming market are expect to grow at a CAGR of +10.3% between 2017 and 2021 with China the biggest market followed by US and Japan. Mobile segment will have the greatest growth as basically everyone owns a smartphone. (Source) In Southeast Asia the market is also gaining momentum as PC Online and mobile gaming revenue hit over $2.2 billion in 2017

with expectations that it will reach over $4 billion by 2021. The

number of PC online and mobile gamers in SEA is projected to reach 300 million by the end of 2017, rising to more than 400 million by 2021. (Source) [This why Singtel want a piece of the pie]

China Freeze on New Games In

August, China has halted approval of new games while the regulators are

amid an internal restructuring. Twitch was banned in the following

month and of any e-sport broadcast. All these in order to control the

addiction and health of the minors. Ironically, China sent a team to the 18th

edition of the Asian Games held in Jakarta, Indonesia and won quite a number of medals. The 2022 Asian Games is also to be held in Hangzhou. Impact of China Limited Logically,

halting of new games won't stop the growth of the China gaming market.

There are still popular games in the market, gamers just need to choose

from the current library. Hence the market can still grow just that the

gamers can't access to new games. However I doubt China will freeze indefinitely. Especially so that the 2022 Asian Games will be held in Hangzhou. How

can China control the access to games? Unless the regulator can control

the hours a person can get access to a game as they had mentioned. But

can the regulator implement that? There will be tons of loopholes, like

using another person devices, fake profiles, etc. In

terms of global growth, China represent 28% of the market, there is

still 72% unaffected. E-sport is also gaining popularity in South East

Asia. Although some game stocks are down, they are still trading near/higher than 20x PE.

IGG successfully transited for a browser based/client based game developer to a mobile game developer that focuses on developing,

producing and licensing games that are free to play with revenue

generation coming from in-app purchases and also live streaming service. IGG first ported games from browser/client based game to mobile and their R&D produced 30 to 50 games a year. In 2013 IGG produced it first hit game Castle Clash, after 4 years is still generating stable revenue. In 2016, IGG's mega hit , Lord Mobile gain tremendous popularity. A result of IGG's marketing into worldwide. IGG's registered IP address from over 200 countries, playing their games. IGG diversify by marketing and producing its games into different languages, to different countries and tap into different talent pool. Limiting its reliance/exposure any country or region. IGG is headquartered in SIngapore.

Some of IGG games, all have good ratings

Growth Factor I believe Lord Mobile still has room to growth as it has not plateau yet like Castle Clash.Up coming games such as Castle Clash 2 will help with growth. IGG empathizes on/setup R&D in different regions should helps build on their success to produces to produce better quality games. Lord Mobile was launched 3 years after Castle Clash. Let's hope IGG can repeat the same success. Growth: Live Streaming I

had read the past 6 years of the annual reports but not a word was

mentioned of the live streaming subsidary. I only discovered that IGG owns a live-streaming

subsidiary when I read the only analyst that is covering IGG at Seeking

Alpha. The subsidiary is call PocketSocial, the live-streaming platform is called

StreamCraft. StreamCraft was just released in early 2018. According to

the Google Play Store, it has over 100,000+ downloads and over 5,000 reviews with a 4.5 star average. As

per article mentioned, most investors like myself will miss out this

potential catalyst if not for reading the article. Just like Twitch, if

successful, provide recurring income from advertisement, subscriber just

like Twitch. Hence this part of IGG's business is likely not priced in IGG’s current stock price.

Streamcraft

StreamCraft

Business Risk Risk involve making a hit games that may or may not happen as the gaming market is highly competitive, the app store drowned with games. Even though a game became a hit, how long the can the game remain relevant as gamers get bored remain to be seen. However IGG has manage to make 2 hit games so far in their 6th year as a game developer IGG's first hit, Castle Clash well into its 6th years, extending its lifespan by regularly introducing new game features, rapidly resolving technical issues, and consistently providing excellent customer service, to build a large community of loyal gamers.

Business Moat Popular,

fun games with loyal gamers is a moat for any games. Once a gamer is

devoted into a game, he will stick around for a long time. Especially

truth for pay to win, If gamers(like me) who will only play for free

will totally avoid or quit the game in a short period of time. As long

there is new content and the gamers are happy, the game will be keep

alive and hence recurring revenue. However this moat may not last long, depend on the game popularity, like World of Warcraft, 14 years running (Apparently starting to fail with crappy content being released). But if IGG is able to build on a library of popular games that can last 14 years, recurring income will be huge, IGG as a mobile developer is only 5+ years old.

A Youtube Search Tell You How Popular the Gamer Is

Temasek Holdings Temasek Holdings owns IGG through Vertex since pre-IPO. It has stake of about 9.1%, read from a 2014 article. Not sure if they are still holding on to it. Conclusion IGG is a relatively young company consider that is transited to a mobile developer in 2013, till now is only 5+ years. Compare to well known brands and IP like Blizzard, Capcom, Final Fantasy, there is no wonder IGG is seen as higher risk, hence the low PE. However, IGG is generating a lot of FCF, paying a nice dividend yield of 5.56% at current price of HKD8.81. It also has a strong balance sheet with no debt, current ratio is way above 1x. Riding on the growth of mobile gaming market, I believe IGG will continue to grow with the current hit, Lord Mobile and up coming games such as Castle Clash sequel. I will need to pay attention to its performance. You can read Seeking Alpha analyst report on IGG here.

I have been eyeing on Frasers Commercial Trust(FCOT) for awhile since I divested CapitaCommercial Trust back in 2017. However the news of Hewlett-Packard moving out of FCOT hold me back. I was informed recently that my office is moving to Alexandra Technopark. This prompt me to take a fresh look on the REIT. Alexandra Technopark I believe Hewlett-Packard risk has been fully priced in. Hewlett-Packard now only occupy 3.7% of gross rental income of FCOT portfolio. AEI on Alexandra Technopark to be finished 2H2018, got some new

facilities and exercise areas. Too bad no gym doh. Assuming Alexandra Technopark will continue to attract tenants, this is a catalyst for DPU growth.

55 Market Street Divestment After the divestment completion in Aug 31 2018, gearing is reduce to 26.5% assuming proceeds are used to pay down debts. This allows more rooms for acquisition, RORF from sponsor Frasers Property. NAV pro forma is $1.70 as at 30 sept 2017, adjusted to current price, NAV should be $1.60. At current price of $1.41, PB ratio is 0.88.

Conclusion The completion of AEI at China Square Central and Alexandra Technopark (as well as tenant growth) will be near

term catalyst. In addition there will be room for more acquisitions.

However, management fees are 100% paid in

units compare to 12% in 2017. Reversing this may halt DPU growth but

remain stable. In 2Q2018, 1,884,606 units were issued at $1.4192 as

management fees worth $2.675 Million which is equivalent to $0.031 per

unit if taken in cash. DPU for the pass few years has been stagnant, probably due to FCOT' plans for Hewlett-Packard's departure as well as the cost for the AEI. At DPU of 9.6cents, current price of $1.41 give a yield of 6.81%. With adjusted pro forma of $1.60, PB ratio 0.88. Assuming a yield of 7%, TP to be set at $1.37 or below. I believe the worst is over for FCOT.

An Edge Singapore article " Airport a proxy to Asia's rising middle

class" sparked my interest in the airport business. (You can read a short

Edge article here). If only Chang Airport is listed, I will definitely invest, a better option than SIA and maybe SATS.

The

International Air Transport Association (IATA) expects 7.8 billion

passengers to travel in 2036, a near doubling of the 4 billion air

travelers expected to fly this year. The prediction is based on a 3.6%

average Compound Annual Growth Rate.

Singapore just opened T4 and is planning for T5 to prepare for the growth in air traffic.

When T5 is completed by 2030, it will increase

Changi’s annual capacity by 50 million passengers initially and up to

70 million if needed – which would mean 150 million passengers a year,

compared with the current capacity of 82 million. By the mid-2020s, China is set to become the

world’s biggest aviation market and India the third largest. By 2035,

the number of people flying to, from and within China and India will be

1.3 billion and 442 million respectively. (Source)

Here are the PE of some of the airports in the region:

What caught my eye is Beijing Capital Airport , the world 2nd most busiest airport.The current low PE is due to:

Exclusion of booking airport fees as revenue in its books from Nov 2018

Capacity overload, the airport is running over its max capacity. Hence growth is limited.

Beijing Daxing Airport to be operational 2H2019. Some airlines will be shifted from Beijing Capital Airport. Expecting a decline in revenue due to the shift.

Beijing Capital Airport is trading at great discount compared to its

peers. As reason stated above, 30% of Beijing Capital Airport's revenue

will be affected, therefore the adjusted PE can be estimated to be

18.16x, calculated with 70% of current EPS. In comparison, Beijing Capital Airport is trading at a very cheap valuation. But expect short term impact from transiting into “one city, two airports”.

NOTE: All Value in RMB other than NAV.

Beijing Capital Airport non-aeronautical business has growth substantially, while the aeronautical business is growing well but limited to its capacity.

The aeronautical business includes the following:

Provision of aircraft landings and take-offs and passenger service facilities,

Ground support services

Firefighting services for domestic and foreign air transportation enterprises.

Non-aeronautical business includes the franchise-based operation of:

Ground handling agent services supplied for domestic and foreign airliners

In-flight catering services

Duty free and other retail shops in the terminals (rental and a cut in profits)

Restaurants and other catering businesses in the terminals

Leasing of advertising spaces inside and outside the terminals and other businesses at Beijing Capital Airport.

Leasing of properties in the terminals

Car parking services

Ground handling facilities for ground handling agent companies.

With the opening of Beijing Daxing Airport, the aeronautical business segment will shrink, probably to 38% if this segment is to affected by 30%.

Business Moat

Business moat for running an airport is super high. Running an airport requires license from the state hence usually are state run. Each airport also build to serve a particular region, due to land and environment constraint. It is unlikely to build multiple airports near one another. This provide a monopoly for the airport business.

Growth Factor

Short term, growth will be hammered down thus the low PE. Longer term, Beijing Capital Airport will continue

to grow and has the option to buy over Beijing Daxing Airport from its

parent company when the new airport matures.

Business Risk

Economic slowdown will hamper growth at a slower rate. Logically, air traffic will increase over the long term as more people can afford to travel, just like more people buying cars or use private hires like Grab and Uber.

Conclusion

Beijing Capital Airport current payout 40% of its earnings, giving a current yield of 3.16%. Not in the best shape with current ratio lesser than 1 but from the

chart, it show that debt is being repaid and current ratio has gradually

recovered. DBS Research projected debt to be fully repaid by end of 2019, Debt/Equity has come down significantly.

ROE and Net margin has been gradually improved over the years, ROE is above 20% net margin above 10%. Revenue will be affected in in the short term but I believe long term wise aviation will grow. Will be looking forward for Beijing Capital Airport to buy over Beijing Daxing Aiport when it is profitable in the future.

Moreover, China Passport holder amounts to 9% of their population. Even an increase of 1% will increase huge traffic growth. The same can also be said to the tourism industry or hotels. This investment is for the long term, I am expecting a minimal of 10 years. As I think airports still a necessity for a nation/state for traveling world wide even if automated plane took over. Manufacturer or service provider companies may get disrupted. Just today I read that Serial System loses Texas instrument distribution agreement which affect 50% of its revenue. I am Vested at HKD8.063, HKEX:694