Hey, not all business huat all the time. If not just buy a stock await for it to fly every year. Just as Warren Buffet say, guidance for every quarter bring more harm than good as investor only focus on the short term.

With investor spoofed by the guidance, UMS stock price falls to 0.75 from 0.83. I wonder if AMAT performance really affect UMS?

|

| In Millions |

UMS Correlate with AMAT?

AMAT announced poorer foretasted revenues for the next quarter and flat for the following but BofA Merrill Lynch expects the company's semiconductor equipment revenues to drop 15.2% next quarter. So does the performance of AMAT affects UMS?

|

| In Millions |

From What I see only both ends correlate when there is a drastic increase/increase in AMAT revenue.

Hypothesis

Let's say AMAT revenue falls and lasted for a few years and it affected UMS. As long it doesn't become as bad as during GFC, dividend should maintain but share price is another matter.

But I hope market just corrects a bit and then continent business as usual and hopefully IoT will improve UMS earnings

|

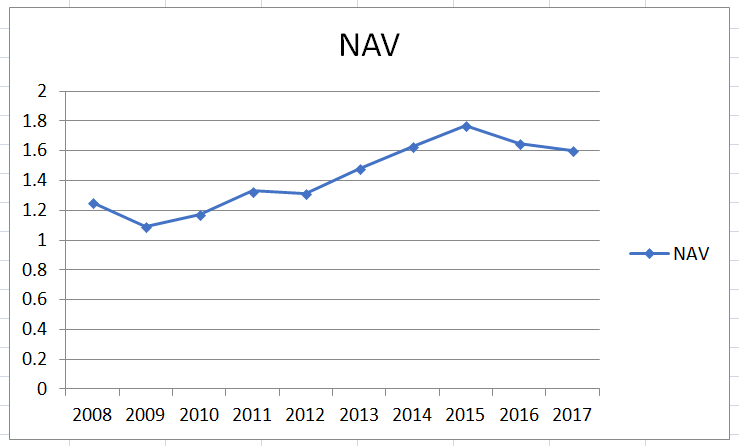

| Hey I can hope that history will repeat right? |

Conclusion

I think UMS dividend can be maintain. Share price however cannot be said to be as certain. It was below 0.50 before 2017. However now that it has been discovered with high dividend, hopefully price can be supported by the dividend.

And AMAT's performance hardly correlate with UMS unless there is a huge change in revenue. let's hope AMAT performance doesn't drop too drastically anytime soon and do not impact UMS earnings. However, Mr. Market would not think it that way.

The latest 2017 also show that as long as AMAT do well in the long run and grow, UMS stands to benefit.

Divest amid deteriorate results and swapping for more able reits for stability